News

Authors: Kilian Moote, Head of US ESG Advisory Services and

Brigid Rosati, Head of US Business Development

Key Takeaways:

In October 2023, California enacted two landmark laws as part of a “Climate Accountability Package.” The “Accountability Package” aims to significantly enhance corporate transparency and accountability in relation to greenhouse gas (GHG) emissions and climate-related financial risks for companies “doing business in California.”[1] These two laws are the Climate Corporate Data Accountability Act (SB-253) and the Climate-Related Financial Risk Act (SB-261). Together, SB-253 and SB-261, represent a critical development for company reporting on climate. While other regulations have been proposed for public companies and companies operating in the EU, the inclusion of private companies differentiates these California laws.[2] [3]

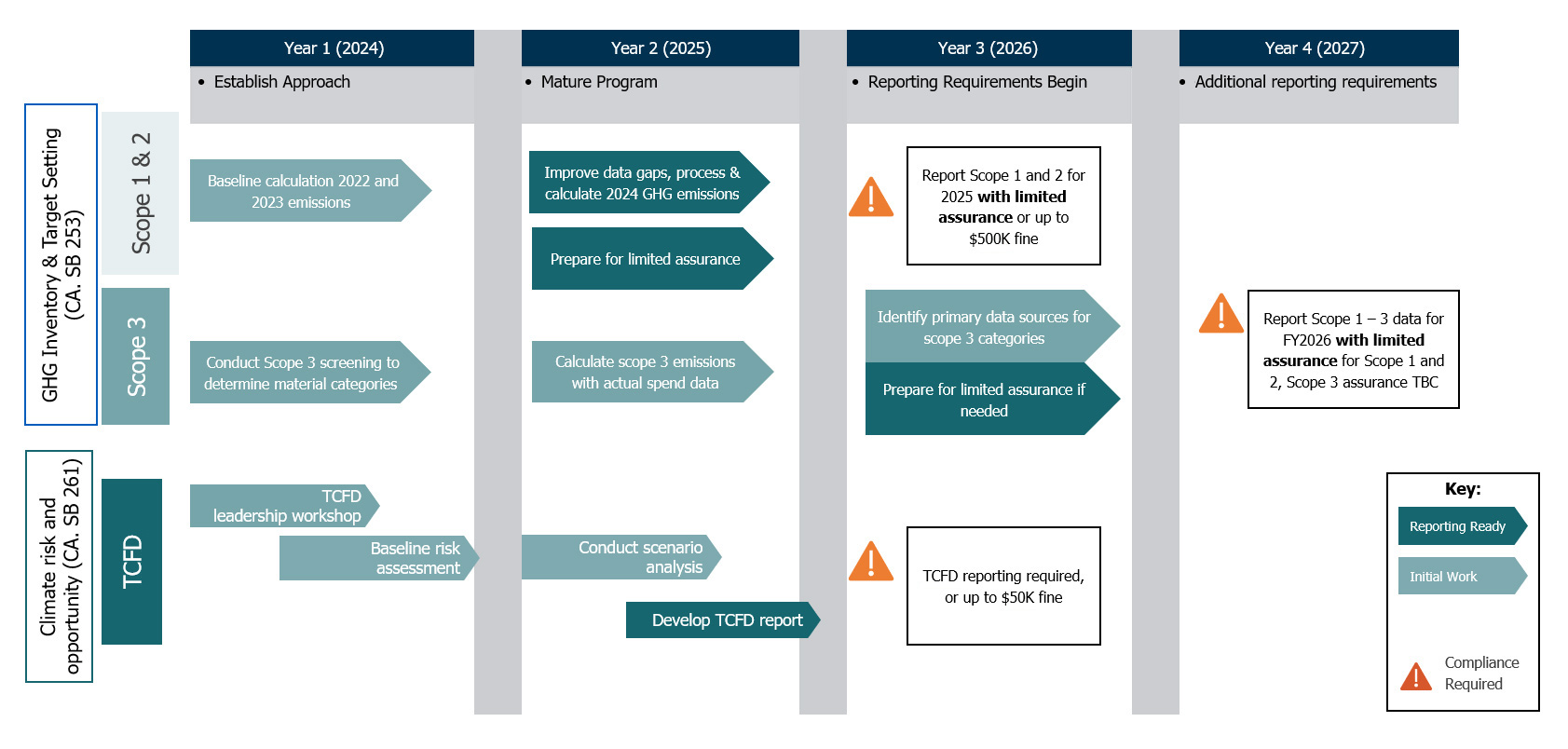

While companies have time before reporting is required, disclosure covers preparation such as collecting granular GHG data, adapting governance and oversight, and conducting climate scenario analysis. For companies not already taking action on these topics it can easily take 24-months. A suggested timeline for action is detailed below for when certain steps should be accomplished.

The Climate Corporate Data Accountability Act (SB-253) mandates that all companies, public and private, doing business in California with over $1 billion in annual revenue disclose their GHG emissions from Scope 1, 2, and 3 sources. The Accountability Act further requires third-party assurance of these disclosures. SB-253 is perceived to be “the strictest corporate emissions disclosure requirements in the U.S. – even stricter than the Securities and Exchange Commission’s (SEC’s) proposed climate disclosure rules.” More than 5,000 companies are expected to be subject to the requirements under SB-253.

Background on Scope 1, 2, and 3:

The reporting timeline for SB-253 is phased in over two years beginning in 2025, providing businesses with a transition period to adapt to the new requirements.

Timeline:

The Climate-Related Financial Risk Act (SB-261) complements the GHG disclosure requirements by mandating that companies (private and public) doing business in California with over $500 million in annual revenue disclose their climate-related financial risks and the measures they are taking to mitigate those risks. This disclosure aligns with the recommendations of the Task Force on Climate-Related Financial Disclosures (TCFD), an industry-led framework for companies to assess and manage climate-related financial risks. The law requires companies to prepare and publicly disclose reports on their climate-related financial risks, including potential physical and transition risks arising from climate change.

More than 10,000 companies are expected to be subject to the requirements under SB-261. First reports are required by January 2026, and biennially thereafter.

Both the SB-253 and SB-261 establish penalties for non-compliance.

This notice is provided by Georgeson for general informational purposes only and is not intended and should not be construed as legal, regulatory, financial or tax advice. Georgeson is not licensed or authorized to practice law in any jurisdictions and hence does not provide any legal advice and it does not hold itself out as doing so. Neither Georgeson nor any of its affiliates or contributors accept any responsibility or liability for the quality, accuracy or completeness of any information contained in this notice. It is important that you seek independent professional advice relating to the subject matter of this notice before relying on it.

1 EUR-Lex - 32014L0095 - EN - EUR-Lex (europa.eu)

2 Corporate sustainability reporting (europa.eu)

3 Mayer Brown, “Are You “Doing Business” in California?,” 2021: Link - mayerbrown.com