On February 4, 2020 Vanguard released its 2020 policy updates which will be applicable to all U.S.-domiciled company meetings held on or after April 1, 2020.

Similar to previous years' policy reports, Vanguard's 2020 voting guidelines continue to be organized in accordance with the four pillars of its Investment Stewardship group.

Georgeson's 2020 policy update focuses on significant changes to Vanguard's voting policies under these four pillars since its prior publication, in 2019. To learn more about Vanguard's 2019 policy, please read Georgeson's prior year report here.

A complete list of Vanguard's 2020 policy guidelines are available at the company's website here.

Pillar I – Board Composition and Effectiveness

Overboarding

Last year, Vanguard's most significant policy update within Pillar I was its updated overboarding policy. Under this policy:

- Vanguard will vote against any director who is a named executive officer (NEO) and sits on more than one outside public board.

- Vanguard will also vote against any director who serves on more than four public company boards.

This year, Vanguard has modified its policy. Consequently, the investor will now consider voting in favor of a director, who would otherwise be considered overboarded because of company-specific facts that indicate the director will "indeed have sufficient capacity to fulfill his/her duties."1

Board and committee independence

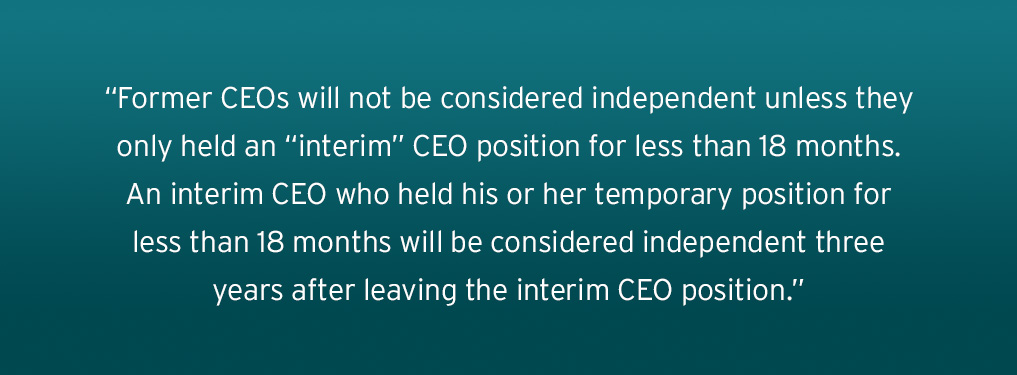

Vanguard states it will continue to vote against the nominating committee and all non-independent directors if the company's board is not comprised of a majority independent directors. However, this year it has clarified its policy on the independence of former CEOs serving on the board.2

This year, Vanguard has sharpened its position on committee independence, stating that if any committee is not 100% independent it will vote against the nominating committee chair.

Board responsiveness

In its 2020 policy report, Vanguard states it will vote against the compensation committee chair where "egregious pay practices are identified." Previously, Vanguard's policy on this topic had referenced voting against the entire committee if pay practice issues persisted over time.

Pillar II - Oversight of Strategy and Risk

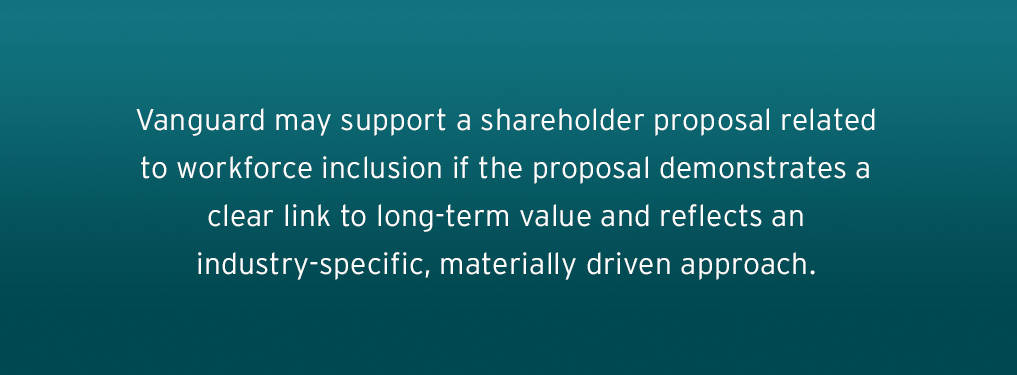

Workforce inclusion

This year, Vanguard has added language to support its view of the board's oversight of key workforce risks and strategies, which it believes can be a component of long-term shareholder value.

Pillar III – Compensation

Absolute limits

Under its updated policy, Vanguard will no longer vote against executive compensation proposals with absolute limits. However, it will still consider the use of absolute metrics as a warning sign or "yellow flag" when reviewing executive compensation plans.

Pillar IV – Governance Structures

Special Meeting Shareholder Proposals

Vanguard's policy now states it will vote against shareholder proposals seeking to lower ownership threshold below the company's current threshold; previously its policy was to vote against proposals to lower the threshold below 25%.

If you have questions or comments, please email info@georgeson.com or call 212 440 9800.

1 "Vanguard funds, Summary of the proxy voting, policy for U.S. portfolio companies," 2020 edition, p. 4

2 "Vanguard funds, Summary of the proxy voting, policy for U.S. portfolio companies," 2020 edition, p. 3